# for QR codes use inline

# %matplotlib inline

# qr_setting = 'url'

# qrviz_setting = 'show'

#

# for lecture use notebook

%matplotlib inline

qr_setting = None

#

%config InlineBackend.figure_format='retina'

# import libraries

import numpy as np

import matplotlib as mp

import pandas as pd

import matplotlib.pyplot as plt

import laUtilities as ut

import slideUtilities as sl

import demoUtilities as dm

import pandas as pd

from importlib import reload

from datetime import datetime

from IPython.display import Image

from IPython.display import display_html

from IPython.display import display

from IPython.display import Math

from IPython.display import Latex

from IPython.display import HTML;

Linear Models¶

# image credit

display(Image("images/Sir_Francis_Galton_by_Charles_Wellington_Furse.jpg", width=550))

HTML(u'<a href="https://commons.wikimedia.org/wiki/File:Sir_Francis_Galton_by_Charles_Wellington_Furse.jpg#/media/File:Sir_Francis_Galton_by_Charles_Wellington_Furse.jpg">Sir Francis Galton by Charles Wellington Furse</a> by Charles Wellington Furse (died 1904) - <a href="//en.wikipedia.org/wiki/National_Portrait_Gallery,_London" class="extiw" title="en:National Portrait Gallery, London">National Portrait Gallery</a>: <a rel="nofollow" class="external text" href="http://www.npg.org.uk/collections/search/portrait.php?search=ap&npgno=3916&eDate=&lDate=">NPG 3916</a>')

{kind=link}

display(Image("images/galton-title.png", width=550))

In 1886 Francis Galton published his observations about how random factors affect outliers.

This notion has come to be called “regression to the mean” because unusually large or small phenomena, after the influence of random events, become closer to their mean values (less extreme).

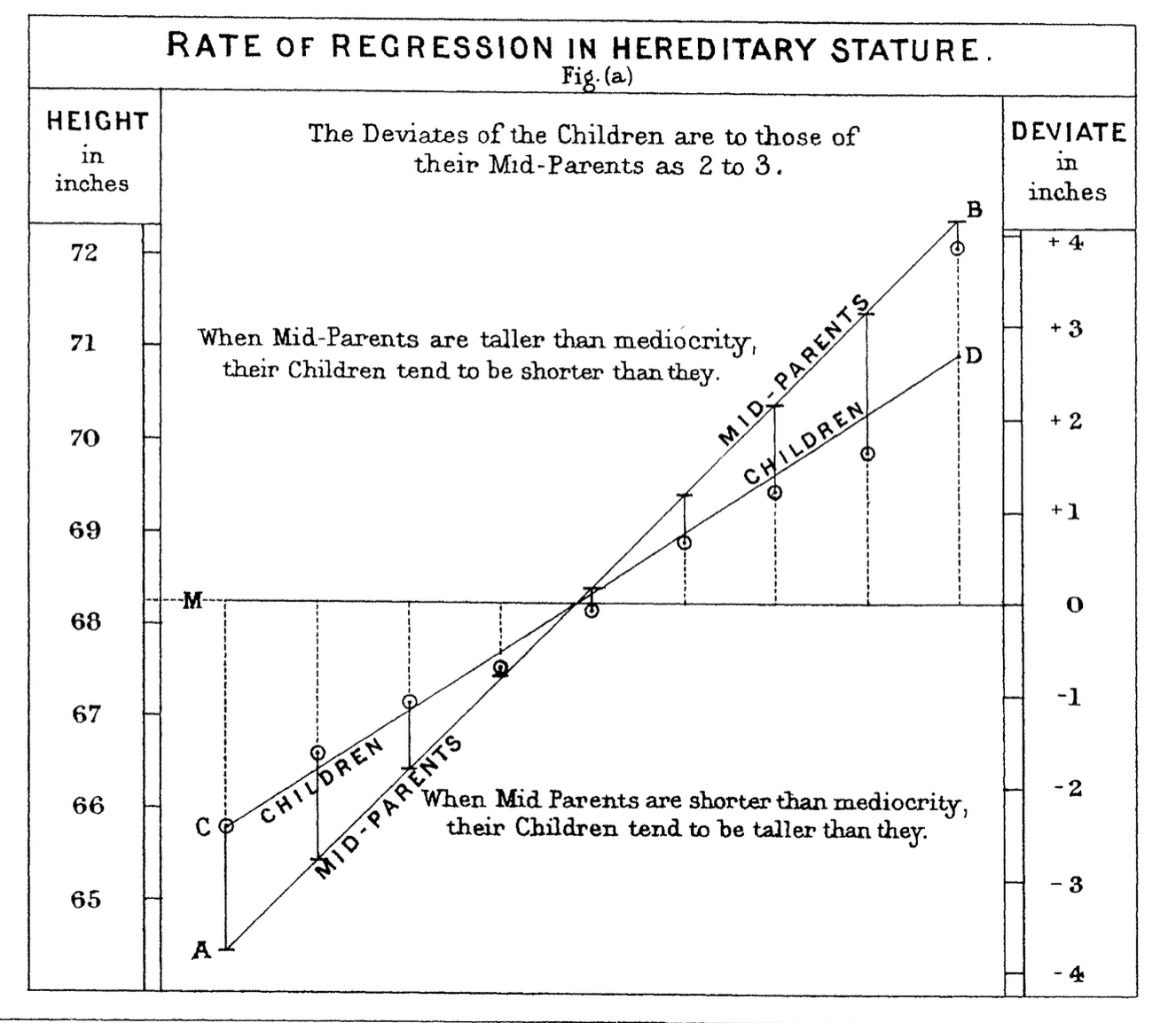

display(Image("images/galton-regression.png", width=550))

One of the most fundamental kinds of machine learning is the construction of a model that can be used to summarize a set of data.

A model is a concise description of a dataset or a real-world phenomenon.

For example, an equation can be a model if we use the equation to describe something in the real world.

The most common form of modeling is regression, which means constructing an equation that describes the relationships among variables.

Regression Problems¶

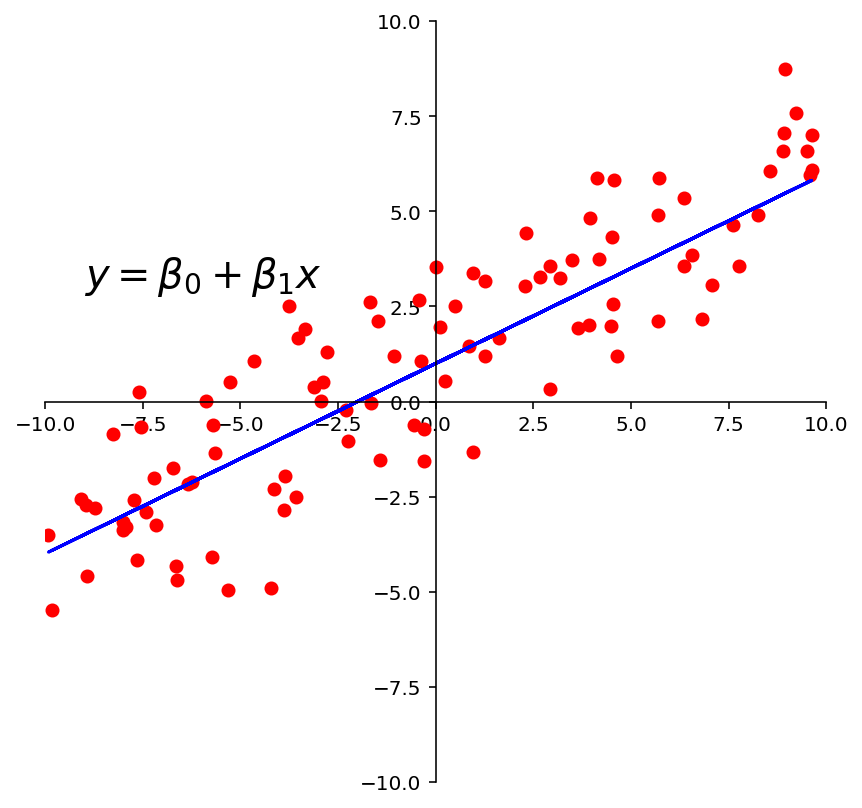

For example, we may look at these points and observe that they approximately lie on a line.

So we could decide to model this data using a line.

ax = ut.plotSetup(-10, 10, -10, 10, size = (7, 7))

ut.centerAxes(ax)

line = np.array([1, 0.5])

xlin = -10.0 + 20.0 * np.random.random(100)

ylin = line[0] + (line[1] * xlin) + np.random.normal(scale = 1.5, size = 100)

ax.plot(xlin, ylin, 'ro', markersize=6);

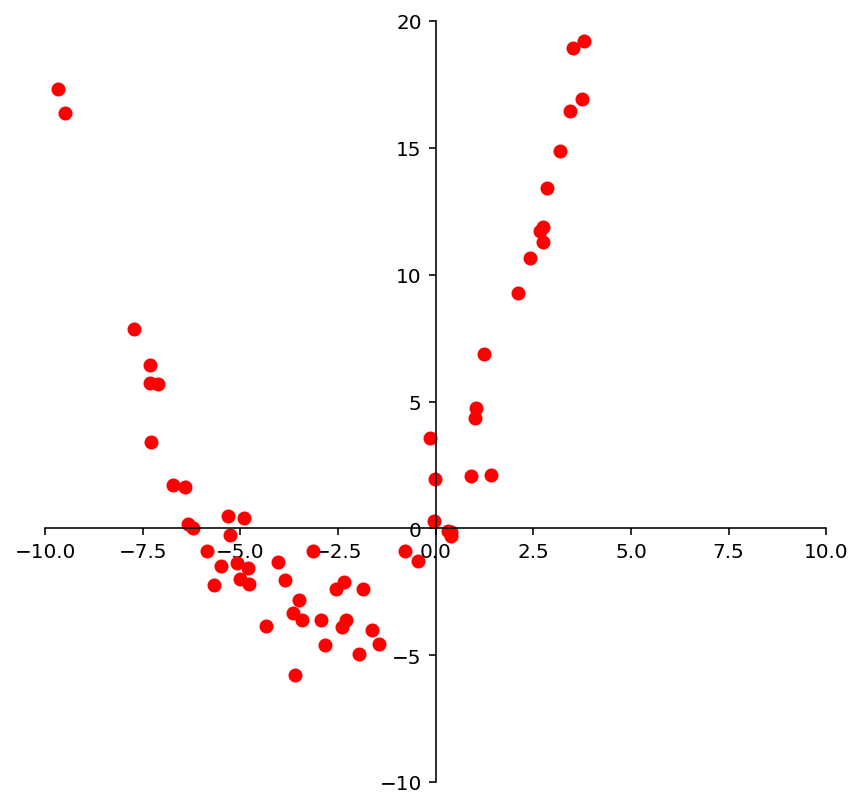

We may look at these points and decide to model them using a quadratic function.

ax = ut.plotSetup(-10, 10, -10, 20, size = (7, 7))

ut.centerAxes(ax)

quad = np.array([1, 3, 0.5])

xquad = -10.0 + 20.0 * np.random.random(100)

yquad = quad[0] + (quad[1] * xquad) + (quad[2] * xquad * xquad) + np.random.normal(scale = 1.5, size = 100)

ax.plot(xquad, yquad, 'ro', markersize=6);

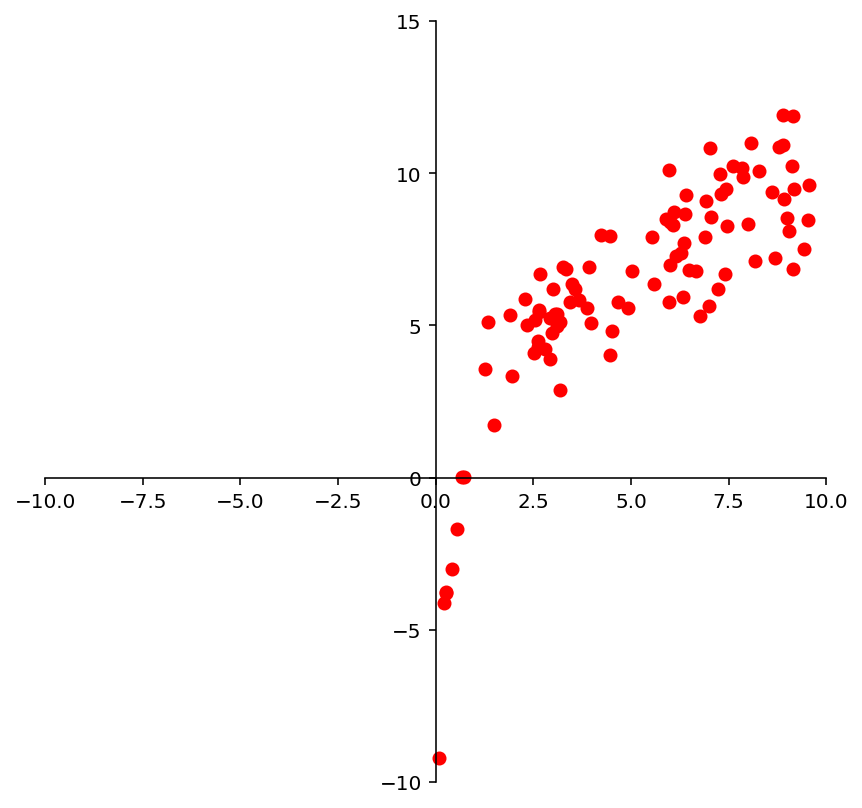

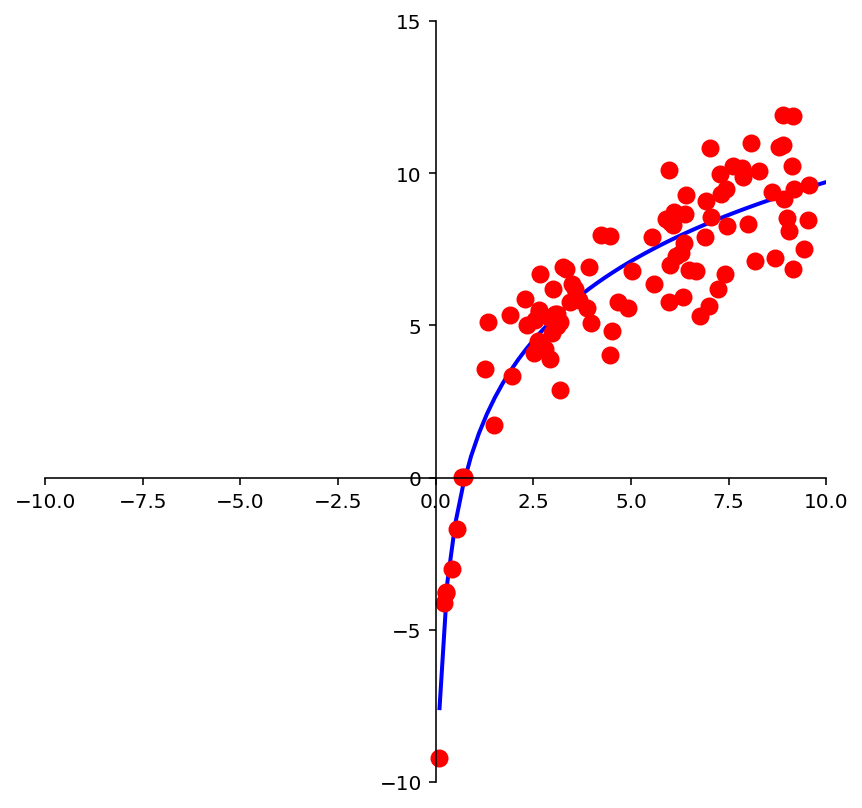

And we may look at these points and decide to model them using a logarithmic function.

ax = ut.plotSetup(-10, 10, -10, 15, size = (7, 7))

ut.centerAxes(ax)

log = np.array([1, 4])

xlog = 10.0 * np.random.random(100)

ylog = log[0] + log[1] * np.log(xlog) + np.random.normal(scale = 1.5, size = 100)

ax.plot(xlog, ylog, 'ro', markersize=6);

Clearly, none of these datasets agrees perfectly with the proposed model. So the question arises:

How do we find the best linear function (or quadratic function, or logarithmic function) given the data?

The Framework of Linear Models¶

The regression problem has been studied extensively in the field of statistics and machine learning.

Certain terminology is used:

Some values are referred to as “independent,” and

Some values are referred to as “dependent.”

The basic regression task is:

given a set of independent variables

and the associated dependent variables,

estimate the parameters of a model (such as a line, parabola, etc) that describes how the dependent variables are related to the independent variables.

The independent variables are collected into a matrix \(X,\) which is called the design matrix.

The dependent variables are collected into an observation vector \(\mathbf{y}.\)

The parameters of the model (for any kind of model) are collected into a parameter vector \(\beta.\)

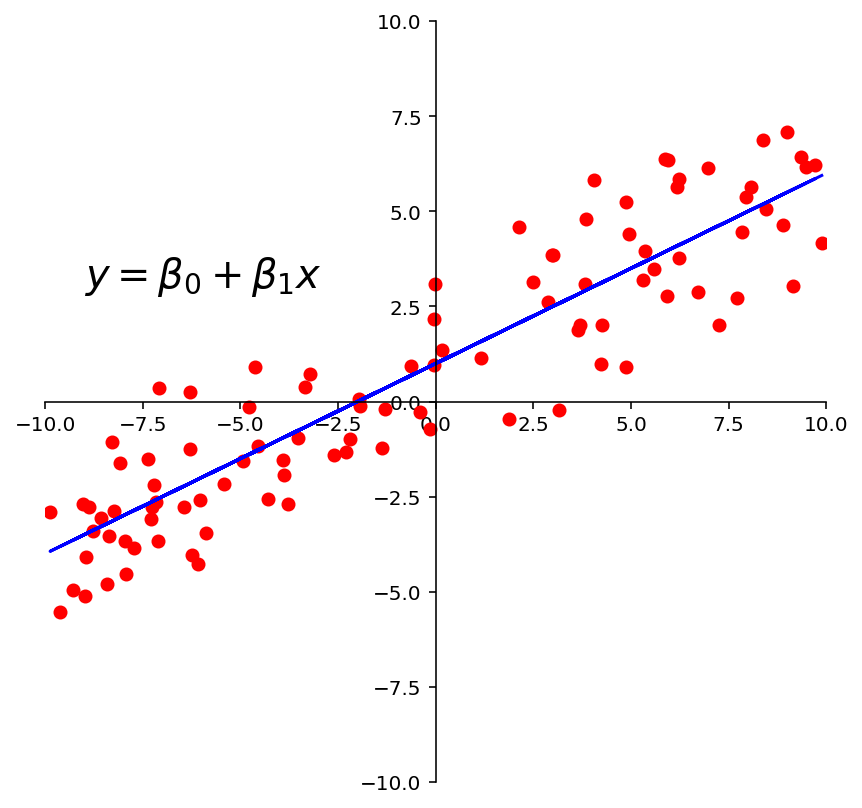

ax = ut.plotSetup(-10, 10, -10, 10, size = (7, 7))

ut.centerAxes(ax)

line = np.array([1, 0.5])

xlin = -10.0 + 20.0 * np.random.random(100)

ylin = line[0] + (line[1] * xlin) + np.random.normal(scale = 1.5, size = 100)

ax.plot(xlin, ylin, 'ro', markersize = 6)

ax.plot(xlin, line[0] + line[1] *xlin, 'b-')

plt.text(-9, 3, r'$y = \beta_0 + \beta_1x$', size=20);

Fitting a Line to Data¶

The first kind of model we’ll study is a linear equation:

This is the most commonly used type of model, particularly in fields like economics, psychology, biology, etc.

The reason it is so commonly used is that, like Galton’s data, experimental data often produce points \((x_1, y_1), \dots, (x_n,y_n)\) that seem to lie close to a line.

The question we must confront is: given a set of data, how should we “fit” the equation of the line to the data?

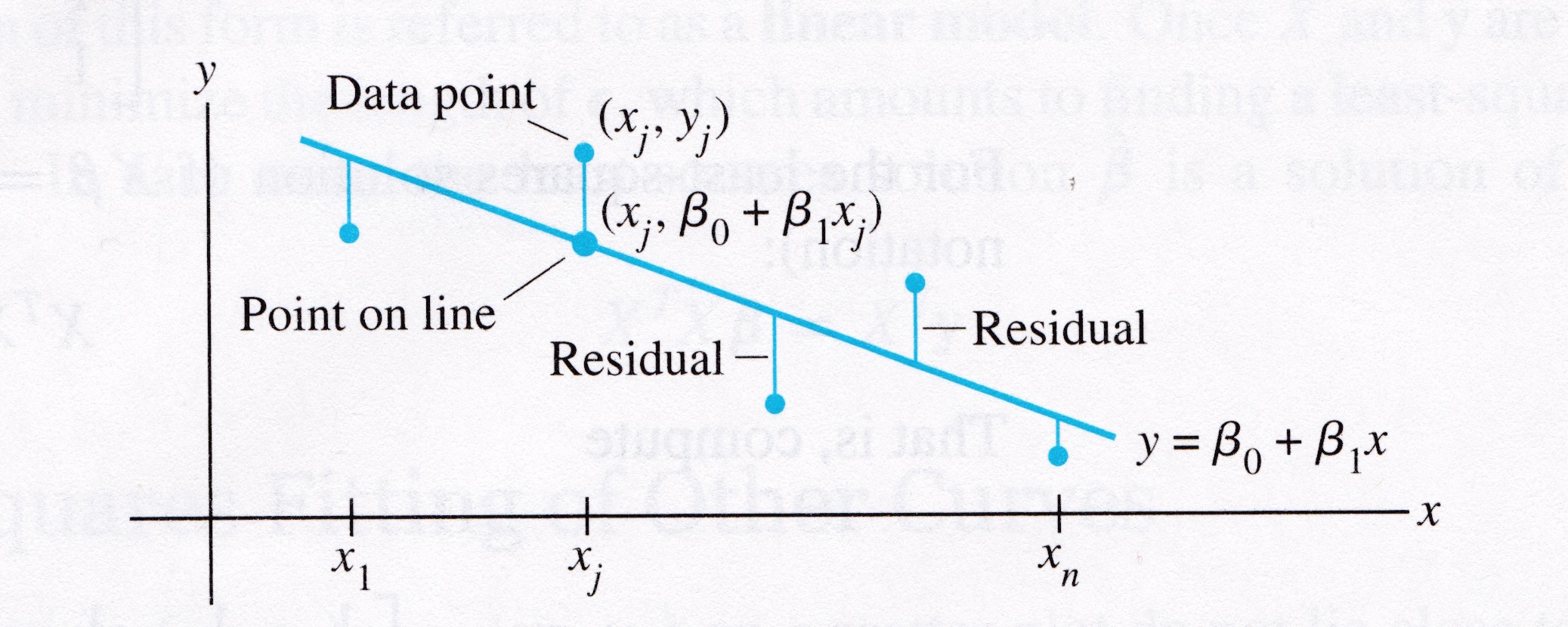

Our intuition is this: we want to determine the parameters \(\beta_0, \beta_1\) that define a line that is as “close” to the points as possible.

Let’s develop some terminology for evaluating a model.

Suppose we have a line \(y = \beta_0 + \beta_1 x\). For each data point \((x_j, y_j),\) there is a point \((x_j, \beta_0 + \beta_1 x_j)\) that is the point on the line with the same \(x\)-coordinate.

# image credit: Lay, LAA, 4th edition

display(Image("images/Lay-fig-6-6-1.jpg", width=550))

We call \(y_j\) the observed value of \(y\)

and we call \(\beta_0 + \beta_1 x_j\) the predicted \(y\)-value.

The difference between an observed \(y\)-value and a predicted \(y\)-value is called a residual.

There are several ways to measure how “close” the line is to the data.

The usual choice is to sum the squares of the residuals.

(Note that the residuals themselves may be positive or negative – by squaring them, we ensure that our error measures don’t cancel out.)

The least-squares line is the line \(y = \beta_0 + \beta_1x\) that minimizes the sum of squares of the residuals.

The coefficients \(\beta_0, \beta_1\) of the line are called regression coefficients.

A Least-Squares Problem¶

Let’s imagine for a moment that the data fit a line perfectly.

Then, if each of the data points happened to fall exactly on the line, the parameters \(\beta_0\) and \(\beta_1\) would satisfy the equations

We can write this system as

where

Of course, if the data points don’t actually lie exactly on a line,

… then there are no parameters \(\beta_0, \beta_1\) for which the predicted \(y\)-values in \(X\mathbf{\beta}\) equal the observed \(y\)-values in \(\mathbf{y}\),

… and \(X\mathbf{\beta}=\mathbf{y}\) has no solution.

Now, since the data doesn’t fall exactly on a line, we have decided to seek the \(\beta\) that minimizes the sum of squared residuals, ie,

This is key: the sum of squares of the residuals is exactly the square of the distance between the vectors \(X\mathbf{\beta}\) and \(\mathbf{y}.\)

This is a least-squares problem, \(A\mathbf{x} = \mathbf{b},\) with different notation.

Computing the least-squares solution of \(X\mathbf{\beta} = \mathbf{y}\) is equivalent to finding the \(\mathbf{\beta}\) that determines the least-squares line.

ax = ut.plotSetup(-10, 10, -10, 10, size = (7, 7))

ut.centerAxes(ax)

line = np.array([1, 0.5])

xlin = -10.0 + 20.0 * np.random.random(100)

ylin = line[0]+ (line[1] * xlin) + np.random.normal(scale = 1.5, size = 100)

ax.plot(xlin, ylin, 'ro', markersize=6)

ax.plot(xlin, line[0] + line[1] * xlin, 'b-')

plt.text(-9,3,r'$y = \beta_0 + \beta_1x$',size=20);

Question Time! Q23.1

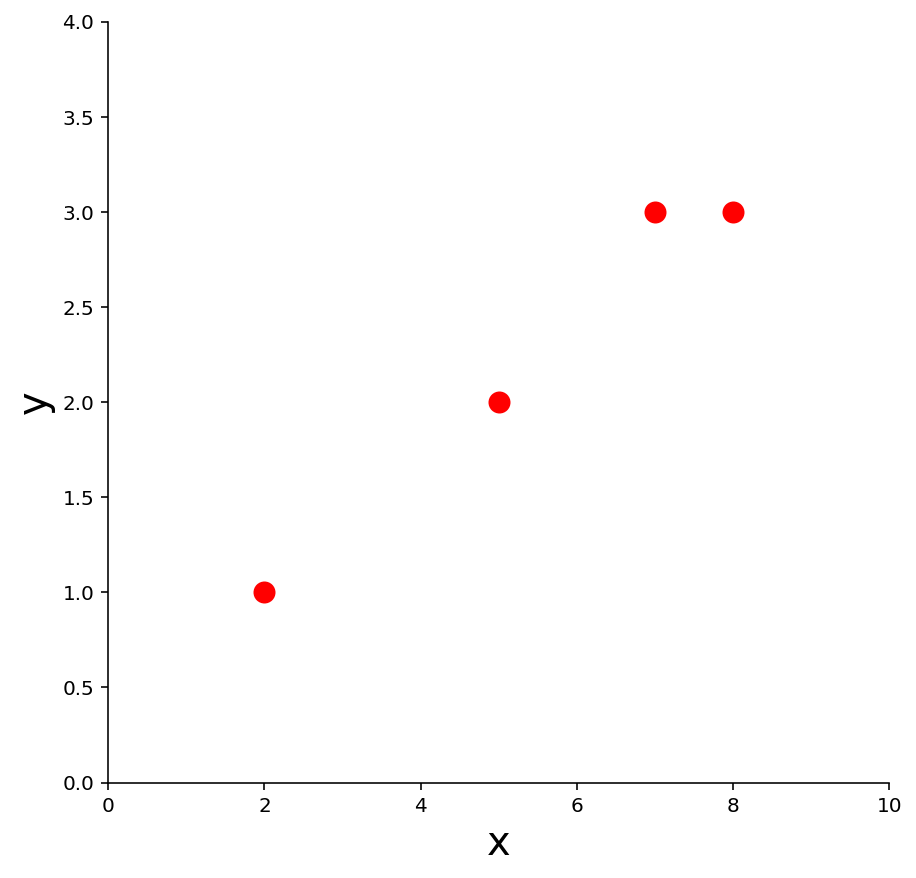

Example 1. Find the equation \(y = \beta_0 + \beta_1 x\) of the least-squares line that best fits the data points

x |

y |

|---|---|

2 |

1 |

5 |

2 |

7 |

3 |

8 |

3 |

ax = ut.plotSetup(0, 10, 0, 4, size = (7, 7))

ut.centerAxes(ax)

pts = np.array([[2,1], [5,2], [7,3], [8,3]]).T

ax.plot(pts[0], pts[1], 'ro', markersize = 10);

plt.xlabel('x', size = 20)

plt.ylabel('y', size = 20);

Solution. Use the \(x\)-coordinates of the data to build the design matrix \(X\), and the \(y\)-coordinates to build the observation vector \(\mathbf{y}\):

Now, to obtain the least-squares line, find the least-squares solution to \(X\mathbf{\beta} = \mathbf{y}.\)

We do this via the method we learned last lecture (just with new notation):

So, we compute:

So the normal equations are:

Solving, we get:

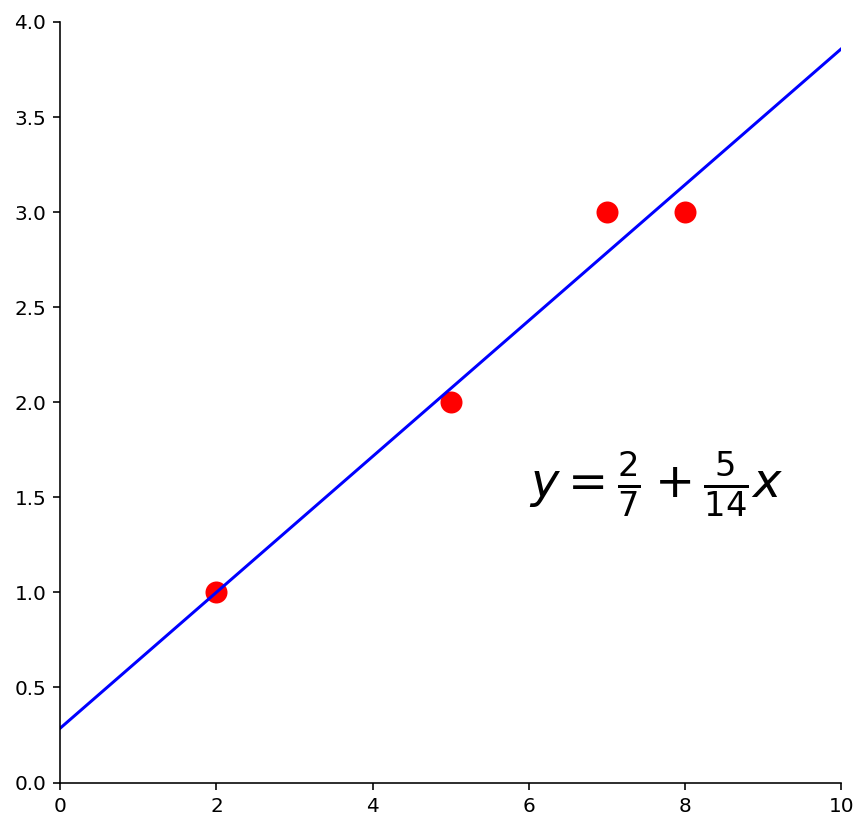

So the least-squares line has the equation

ax = ut.plotSetup(0, 10, 0, 4, size = (7, 7))

ut.centerAxes(ax)

pts = np.array([[2,1], [5,2], [7,3], [8,3]]).T

ax.plot(pts[0], pts[1], 'ro', markersize = 10)

ut.plotLinEqn(-5./14, 1, 2./7, color='b')

plt.text(6,1.5, r'$y = \frac{2}{7} + \frac{5}{14}x$', size=24);

The General Linear Model¶

Another way that the inconsistent linear system is often written is to collect all the residuals into a residual vector.

Then an exact equation is

Any equation of this form is referred to as a linear model.

In this formulation, the goal is to minimize the length of \(\epsilon\), ie, \(\Vert\epsilon\Vert.\)

In some cases, one would like to fit data points with something other than a straight line.

For example, think of Gauss trying to find the equation for the orbit of Ceres.

In cases like this, the matrix equation is still \(X\mathbf{\beta} = \mathbf{y}\), but the specific form of \(X\) changes from one problem to the next.

The least-squares solution \(\hat{\mathbf{\beta}}\) is a solution of the normal equations

Least-Squares Fitting of Other Models¶

Most models have parameters, and the object of model fitting is to to fix those parameters. Let’s talk about model parameters.

In model fitting, the parameters are the unknown. A central question for us is whether the model is linear in its parameters.

For example, the model \(y = \beta_0 e^{-\beta_1 x}\) is not linear in its parameters.

The model \(y = \beta_0 e^{-2 x}\) is linear in its parameters.

For a model that is linear in its parameters, an observation is a linear combination of (arbitrary) known functions.

In other words, a model that is linear in its parameters is

where \(f_0, \dots, f_n\) are known functions and \(\beta_0,\dots,\beta_k\) are parameters.

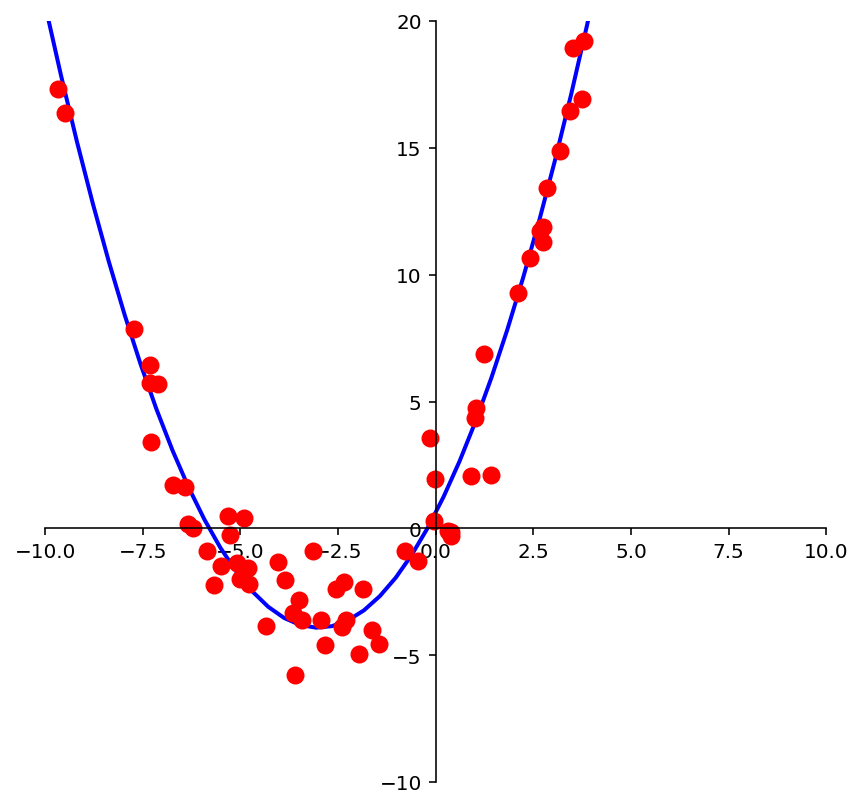

Example. Suppose data points \((x_1, y_1), \dots, (x_n, y_n)\) appear to lie along some sort of parabola instead of a straight line. Suppose we wish to approximate the data by an equation of the form

Describe the linear model that produces a “least squares fit” of the data by the equation.

Solution. The ideal relationship is \(y = \beta_0 + \beta_1x + \beta_2x^2.\)

Suppose the actual values of the parameters are \(\beta_0, \beta_1, \beta_2.\) Then the coordinates of the first data point satisfy the equation

where \(\epsilon_1\) is the residual error between the observed value \(y_1\) and the predicted \(y\)-value.

Each data point determines a similar equation:

Clearly, this system can be written as \(\mathbf{y} = X\mathbf{\beta} + \mathbf{\epsilon}.\)

m = np.shape(xquad)[0]

X = np.array([np.ones(m), xquad,xquad**2]).T

beta = np.linalg.inv(X.T @ X) @ X.T @ yquad

#

ax = ut.plotSetup(-10, 10, -10, 20, size = (7, 7))

ut.centerAxes(ax)

xplot = np.linspace(-10, 10, 50)

yestplot = beta[0] + beta[1] * xplot + beta[2] * xplot**2

ax.plot(xplot, yestplot, 'b-', lw=2)

ax.plot(xquad, yquad, 'ro', markersize = 8);

m = np.shape(xlog)[0]

X = np.array([np.ones(m), np.log(xlog)]).T

beta = np.linalg.inv(X.T @ X) @ X.T @ ylog

#

ax = ut.plotSetup(-10, 10, -10, 15, size = (7, 7))

ut.centerAxes(ax)

xplot = np.linspace(0.1, 10, 50)

yestplot = beta[0] + beta[1] * np.log(xplot)

ax.plot(xplot, yestplot, 'b-', lw=2)

ax.plot(xlog, ylog, 'ro', markersize = 8);

Question Time! Q23.2

Multiple Regression¶

Suppose an experiment involves two independent variables – say, \(u\) and \(v\), – and one dependent variable, \(y\).

A linear equation for predicting \(y\) from \(u\) and \(v\) has the form

Since there is more than one independent variable, this is called multiple regression.

A more general prediction equation might have the form

A least squares fit to equations like this is called a trend surface.

In general, a linear model will arise whenever \(y\) is to be predicted by an equation of the form

with \(f_0,\dots,f_k\) any sort of known functions and \(\beta_0,...,\beta_k\) unknown weights.

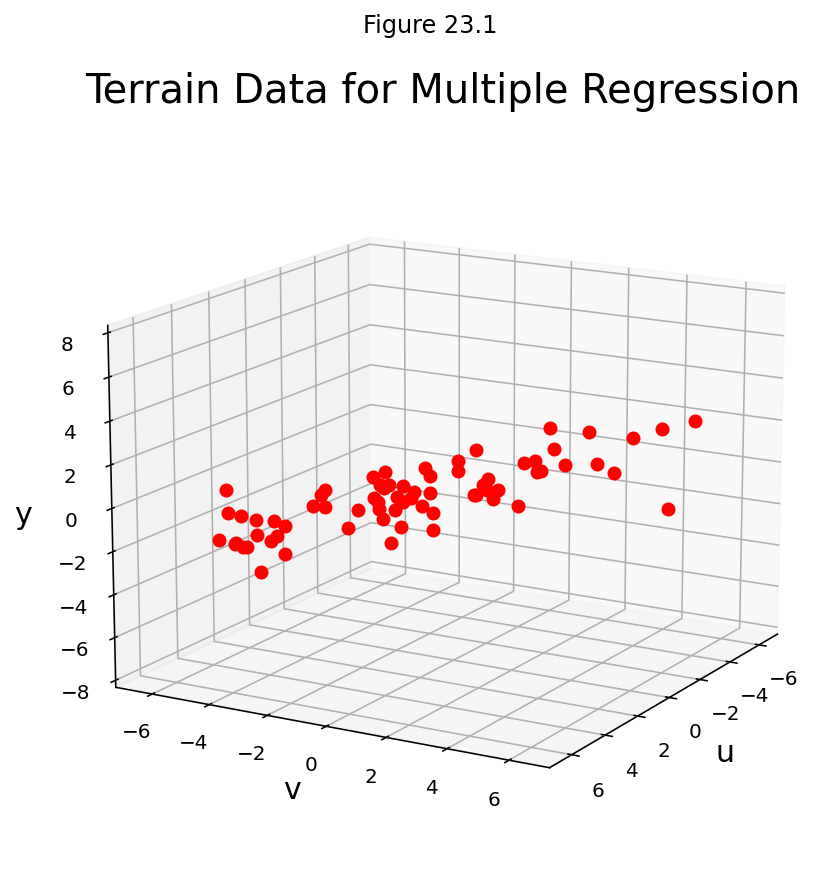

Example. In geography, local models of terrain are constructed from data \((u_1, v_1, y_1), \dots, (u_n, v_n, y_n)\) where \(u_j, v_j\), and \(y_j\) are latitude, longitude, and altitude, respectively.

Let’s take an example. Here are a set of points in \(\mathbb{R}^3\):

fig = ut.three_d_figure((23, 1), 'multivariate regression example',

-7, 7, -7, 7, -8, 8,

equalAxes = False, figsize = (7, 7), qr = qr_setting)

np.random.seed(6)

v = [4.0, 4.0, 2.0]

u = [-4.0, 3.0, 1.0]

npts = 70

# set locations of points that fall within x,y

xc = -7.0 + 14.0 * np.random.random(npts)

yc = -7.0 + 14.0 * np.random.random(npts)

A = np.array([u,v]).T

# project these points onto the plane

P = A @ np.linalg.inv(A.T @ A) @ A.T

coords = P @ np.array([xc,yc,np.zeros(npts)])

coords[2] += np.random.normal(scale = 1, size = npts)

for i in range(coords.shape[-1]):

fig.plotPoint(coords[0,i],coords[1,i], coords[2,i], 'r')

fig.set_title('Terrain Data for Multiple Regression', 'Terrain Data for Multiple Regression', size = 20)

fig.ax.set_zlabel('y')

fig.ax.set_xlabel('u')

fig.ax.set_ylabel('v')

fig.desc['xlabel'] = 'u'

fig.desc['ylabel'] = 'v'

fig.desc['zlabel'] = 'y'

fig.ax.view_init(azim=30, elev = 15)

fig.save();

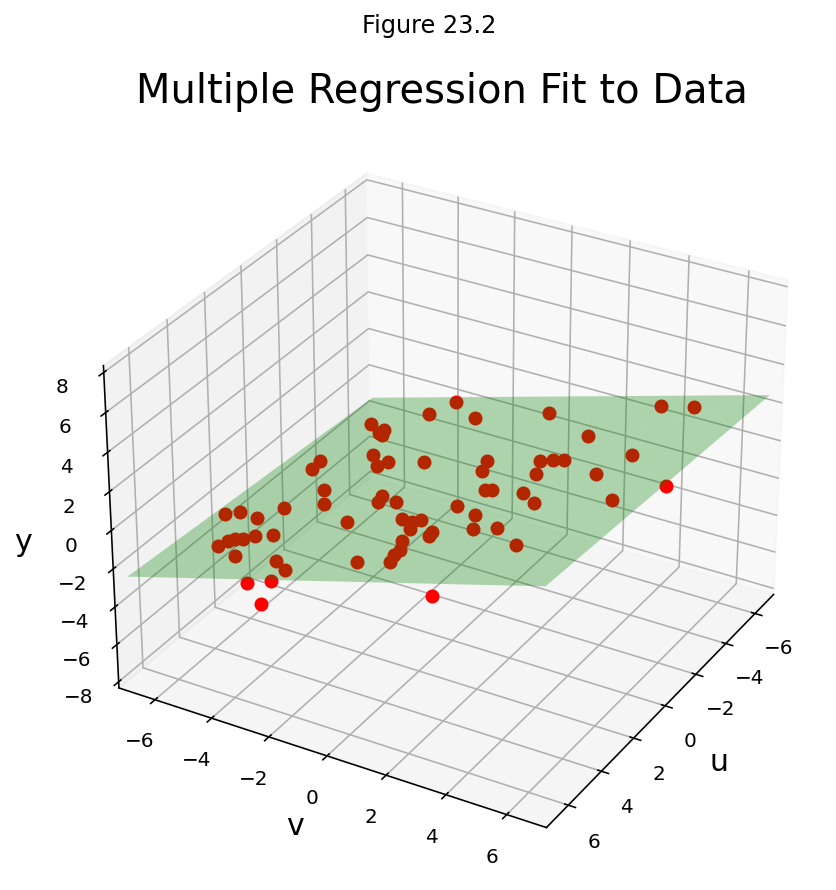

Let’s describe the linear models that gives a least-squares fit to such data. The solution is called the least-squares plane.

Solution. We expect the data to satisfy these equations:

This system has the matrix for \(\mathbf{y} = X\mathbf{\beta} + \epsilon,\) where

fig = ut.three_d_figure((23, 2), 'multivariate regression example with fitted plane',

-7, 7, -7, 7, -8, 8,

equalAxes = False, figsize = (7, 7), qr = qr_setting)

np.random.seed(6)

v = [4.0, 4.0, 2.0]

u = [-4.0, 3.0, 1.0]

npts = 70

# set locations of points that fall within x,y

xc = -7.0 + 14.0 * np.random.random(npts)

yc = -7.0 + 14.0 * np.random.random(npts)

A = np.array([u,v]).T

# project these points onto the plane

P = A @ np.linalg.inv(A.T @ A) @ A.T

coords = P @ np.array([xc,yc,np.zeros(npts)])

coords[2] += np.random.normal(scale = 1, size = npts)

for i in range(coords.shape[-1]):

fig.plotPoint(coords[0,i],coords[1,i], coords[2,i], 'r')

fig.set_title('Multiple Regression Fit to Data', 'Multiple Regression Fit to Data', size = 20)

fig.ax.set_zlabel('y')

fig.ax.set_xlabel('u')

fig.ax.set_ylabel('v')

fig.desc['xlabel'] = 'u'

fig.desc['ylabel'] = 'v'

fig.desc['zlabel'] = 'y'

fig.plotSpan(u, v, 'Green')

fig.ax.view_init(azim=30, elev = 30)

fig.save();

This example shows that the linear model for multiple regression has the same abstract form as the model for the simple regression in the earlier examples.

We can see that there the general principle is the same across all the different kinds of linear models.

Once \(X\) is defined properly, the normal equations for \(\mathbf{\beta}\) have the same matrix form, no matter how many variables are involved.

Thus, for any linear model where \(X^TX\) is invertible, the least squares \(\hat{\mathbf{\beta}}\) is given by \((X^TX)^{-1}X^T\mathbf{y}\).

Multiple Regression in Practice¶

Let’s see how powerful multiple regression can be on a real-world example.

A typical application of linear models is predicting house prices. Linear models have been used for this problem for decades, and when a municipality does a value assessment on your house, they typically use a linear model.

We can consider various measurable attributes of a house (its “features”) as the independent variables, and the most recent sale price of the house as the dependent variable.

For our case study, we will use the features:

Lot Area (sq ft),

Gross Living Area (sq ft),

Number of Fireplaces,

Number of Full Baths,

Number of Half Baths,

Garage Area (sq ft),

Basement Area (sq ft)

So our design matrix will have 8 columns (including the constant for the intercept):

and it will have one row for each house in the data set, with \(y\) the sale price of the house.

We will use data from housing sales in Ames, Iowa from 2006 to 2009:

df = pd.read_csv('data/ames-housing-data/train.csv')

df[['LotArea', 'GrLivArea', 'Fireplaces', 'FullBath', 'HalfBath', 'GarageArea', 'TotalBsmtSF', 'SalePrice']].head()

| LotArea | GrLivArea | Fireplaces | FullBath | HalfBath | GarageArea | TotalBsmtSF | SalePrice | |

|---|---|---|---|---|---|---|---|---|

| 0 | 8450 | 1710 | 0 | 2 | 1 | 548 | 856 | 208500 |

| 1 | 9600 | 1262 | 1 | 2 | 0 | 460 | 1262 | 181500 |

| 2 | 11250 | 1786 | 1 | 2 | 1 | 608 | 920 | 223500 |

| 3 | 9550 | 1717 | 1 | 1 | 0 | 642 | 756 | 140000 |

| 4 | 14260 | 2198 | 1 | 2 | 1 | 836 | 1145 | 250000 |

X_no_intercept = df[['LotArea', 'GrLivArea', 'Fireplaces', 'FullBath', 'HalfBath', 'GarageArea', 'TotalBsmtSF']].values

y = df['SalePrice'].values

Next we add a column of 1s to the design matrix, which adds a constant intercept to the model:

X = np.column_stack([np.ones(X_no_intercept.shape[0], dtype = 'int'), X_no_intercept])

X

array([[ 1, 8450, 1710, ..., 1, 548, 856],

[ 1, 9600, 1262, ..., 0, 460, 1262],

[ 1, 11250, 1786, ..., 1, 608, 920],

...,

[ 1, 9042, 2340, ..., 0, 252, 1152],

[ 1, 9717, 1078, ..., 0, 240, 1078],

[ 1, 9937, 1256, ..., 1, 276, 1256]])

Now let’s peform the least-squares regression:

beta_hat = np.linalg.inv(X.T @ X) @ X.T @ y

What does our model tell us?

beta_hat

array([-2.92338280e+04, 1.87444579e-01, 3.94185205e+01, 1.45698657e+04,

2.29695596e+04, 1.62834807e+04, 9.14770980e+01, 5.11282216e+01])

We see that we have:

\(\beta_0\): Intercept of -$29,233

\(\beta_1\): Marginal value of one square foot of Lot Area: $18

\(\beta_2\): Marginal value of one square foot of Gross Living Area: $39

\(\beta_3\): Marginal value of one additional fireplace: $14,570

\(\beta_4\): Marginal value of one additional full bath: $22,970

\(\beta_5\): Marginal value of one additional half bath: $16,283

\(\beta_6\): Marginal value of one square foot of Garage Area: $91

\(\beta_7\): Marginal value of one square foot of Basement Area: $51

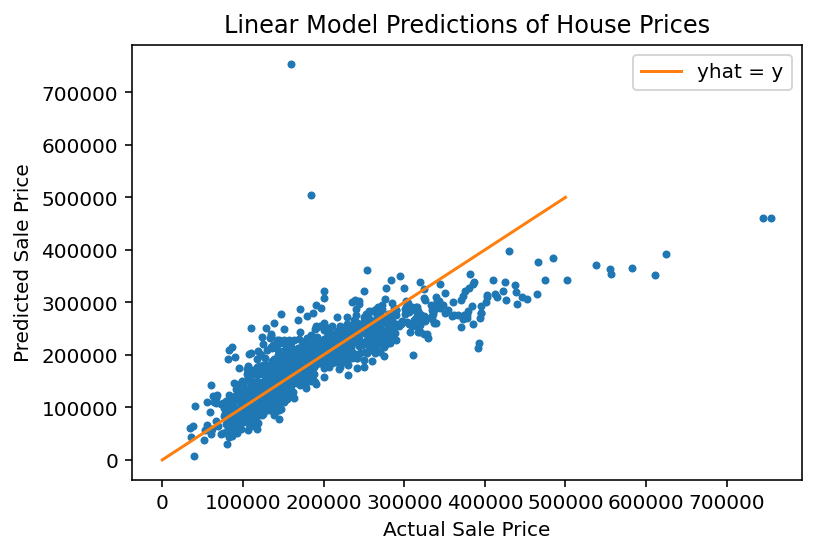

Is our model doing a good job?

There are many statistics for testing this question, but we’ll just look at the predictions versus the ground truth.

For each house we compute its predicted sale value according to our model:

y_hat = X @ beta_hat

And for each house, we’ll plot its predicted versus actual sale value:

plt.figure()

plt.plot(y, y_hat, '.')

plt.xlabel('Actual Sale Price')

plt.ylabel('Predicted Sale Price')

plt.title('Linear Model Predictions of House Prices')

plt.plot([0, 500000], [0, 500000], '-', label='yhat = y')

plt.legend(loc = 'best');

We see that the model does a reasonable job for house values less than about $250,000.

For a better model, we’d want to consider more features of each house, and perhaps some additional functions such as polynomials as components of our model.